India’s core banking solutions get a FinTech makeover – and the shift is redefining the future of banking.

The banking sector in India is witnessing a significant transformation, driven by the symbiotic relationship between FinTech and core banking. Core banking solutions (CBS) have revolutionised Indian banking from its early stages. By streamlining processes and centralising data, CBS has brought efficiency to banking operations. However, to fully meet the evolving needs of consumers, CBS alone has proven insufficient.

Over the past decade, FinTech has stepped in, injecting dynamism and innovation into the traditional banking system. India’s banking landscape is vast and diverse, including the public and private sectors, payment banks, small finance banks, and foreign banks. With twelve public sector banks, 21 private sector banks, 11 small finance banks, and six payment banks, the sector operates with about $2 trillion in assets. Yet, the banking system required more than just CBS to truly flourish.

While CBS brought efficiency and standardisation to banking operations, its limitations became apparent as digital technologies advanced and consumer preferences shifted. This necessitated a more agile, innovative, and customer-centric approach provided by FinTech, which has bridged the gap between traditional banking and the digital era. This FinTech phenomenon is now making significant waves. As financial institutions continue to embrace technology, the potential opportunity for fintech infrastructure is enormous – with the market estimated to grow from $2.7 billion. in 2022 to $20 billion. by 2030.

FinTech companies are reshaping financial services with their agility and customer-centricity. Utilising cutting-edge technologies like AI, machine learning, and blockchain, they create innovative products that cater to the evolving needs of consumers, particularly in underserved segments. FinTech not only complements traditional banking; it elevates it to new heights.

India’s credit growth, hovering around 20%, highlights the pivotal role of FinTech. FinTech lenders have been catalysts for growth in digital lending, focusing on the underserved. They originated loans worth ₹1,107 billion ($13.3 billion) in FY 2022-23. A significant portion of these loans were small-ticket personal loans and consumer durable loans, thereby unlocking credit access for the masses and empowering individuals previously excluded from formal financial services.

The partnerships between FinTech and traditional banks have proven to be a game-changer. Banks are collaborating with FinTech companies to leverage their technological expertise and innovative solutions, leading to the development of new products and services. Examples include mobile banking apps, digital wallets, and peer-to-peer lending platforms, which have significantly enhanced the customer experience and made banking more accessible. Between FY23 and FY24, co-lending volumes have been growing exponentially, with the portfolio growing from ₹25,000 crore. to ₹1 lakh crore.

The Digital Revolution

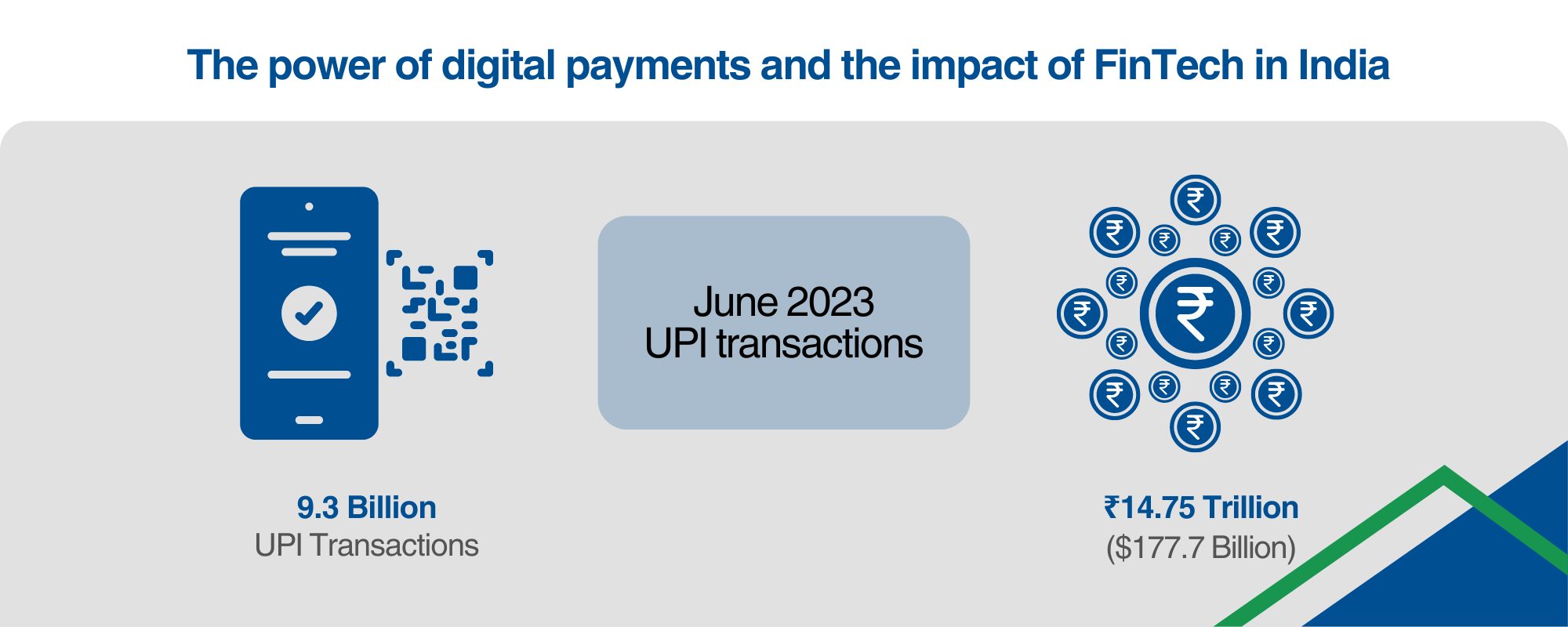

The rise of digital payments has catalysed the FinTech revolution in India. The Unified Payments Interface (UPI), launched by the National Payments Corporation of India (NPCI), has transformed the digital payments landscape. UPI enables seamless and secure transactions, simplifying the process for consumers to make payments and transfer money.

The growth of UPI has been remarkable. Over the last five years, UPI transactions have increased exponentially, demonstrating a 15.5x rise in transaction volumes and a 16x increase in transaction value.

In addition, 36% of digital payment users are from rural India. By 2025, 56% of new internet users in India will come from rural areas. In lending, a significant amount of credit is flowing beyond urban centers—71% of FinTech personal loans originated from beyond Tier-I cities in 2020, presenting a massive opportunity for FinTech companies to drive financial inclusion and tap into untapped market potential.

UPI is just one component of the digital-payments ecosystem. FinTech companies are innovating within this space, offering a variety of solutions such as digital wallets, mobile payment apps, and contactless payments. These solutions are convenient and promote financial inclusion, enabling those without access to traditional banking services to participate in the digital economy.

The digital-payments revolution has also spurred the growth of e-commerce in India. Online shopping and digital transactions have become the norm, particularly among the younger generation. FinTech companies capitalise on this trend by providing seamless payment solutions and integrating with e-commerce platforms, creating a virtuous cycle that drives growth in both digital payments and e-commerce.

FinTech Age

The impact of FinTech on digital payments extends beyond consumer convenience. It has far-reaching implications for the Indian economy, reducing reliance on cash, promoting transparency, and helping curb black money. Additionally, digital payments provide valuable insights that can be used to create targeted financial products and services. Led by FinTech, the digital-payments revolution is transforming India’s financial landscape.

Digital penetration in India has rapidly risen, with 759 million internet users and 667 million smartphones by 2022. This digital adoption is fueling the economy, with social networking driving e-commerce growth. Entertainment, communication, and social media are the top online activities, highlighting the potential for embedding financial services within these platforms.

FinTech is revolutionising not just access to credit but also the methods of credit assessment and analysis. With data analytics and machine learning, FinTech companies can assess creditworthiness in real time, enabling faster and more accurate lending decisions. This shift is creating a more inclusive financial ecosystem where credit is accessible to more individuals and businesses. Tech-enabled processes have brought significant efficiencies to the banking system—the turnaround time (TAT) for personal loan account openings has reduced by 95%, and the cost of processing both secured and unsecured loans has decreased by 45% and 65%, respectively.

As FinTech continues to evolve, it cuts through the layers of complexity and bureaucracy associated with traditional financial services. With just a few clicks on a smartphone, individuals can access a plethora of financial products and services, from savings and investments to insurance and wealth management. This convenience and accessibility are driving the adoption of FinTech solutions across the country.

Furthermore, FinTech is poised to take the country to new heights in financial inclusion, economic growth, and innovation. The symbiotic relationship between FinTech and traditional banking is creating a more robust and resilient financial system capable of withstanding challenges and seizing opportunities.

In summary, the FinTech phenomenon is unleashing India’s financial potential by democratising access to credit, driving payments, and enabling more innovation across the economy. With the increasing digitization of financial services delivery, banks and NBFCs are expected to significantly increase their technology spending to support this digital scale—banks are projected to spend over ₹3.4 trillion by 2034.

It’s no surprise, then, that India has emerged as the third largest FinTech ecosystem globally, with over 1,500 FinTech companies operating in the country. The FinTech ecosystem has evolved rapidly, driven by the entry of payment FinTechs, lending startups, and MSME FinTechs. This shift was accelerated by the convergence of mega trends such as rising digital penetration, a large young population, and increasing per capita income . In the FinTech era, traditional banking, as we know it, has entered a new phase of growth.