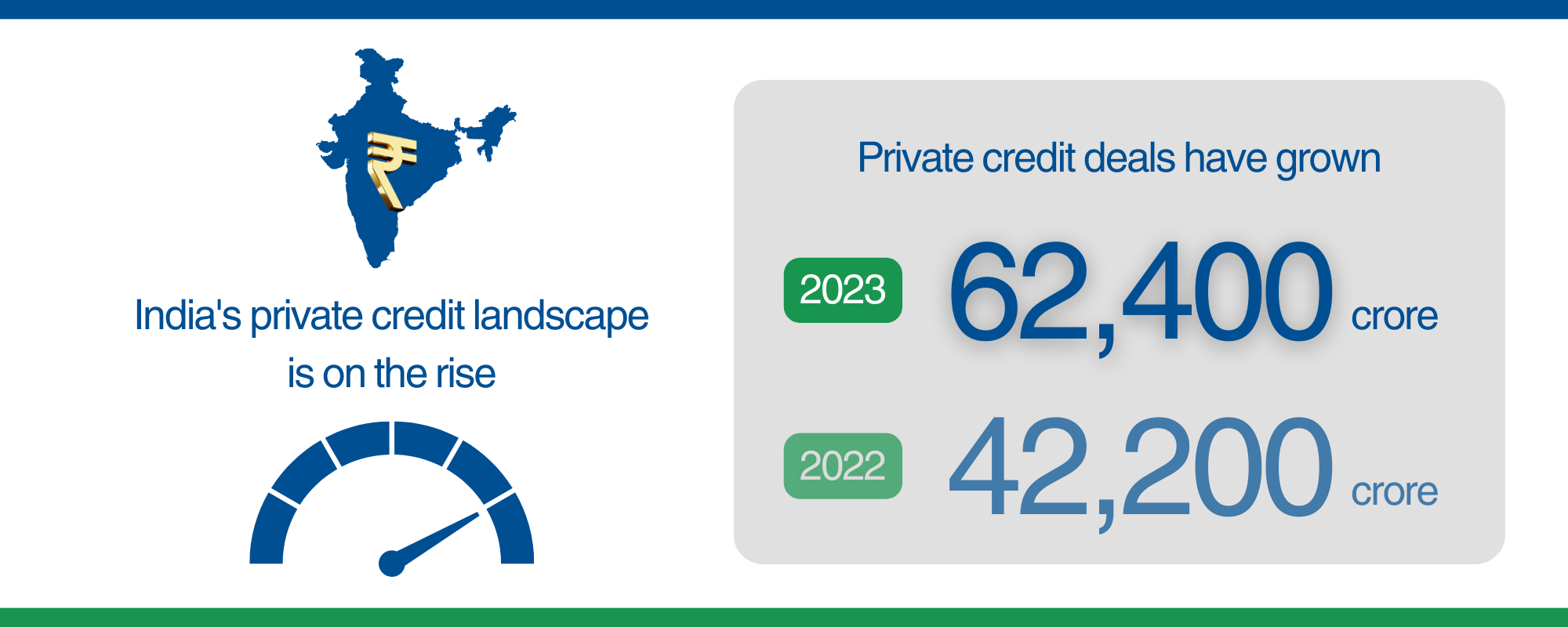

Looking globally, the private debt market has been booming for the last decade. The private debt market stands at an AUM of $1.3 trillion. as of 2022, up 12% from the previous year. The asset class continues to garner significant investor interest, with private debt fundraising standing at $230 billion. over 2023. The market’s need for financing outside traditional banks and the asset class’s attractive returns drove this growth.

More recently, the US (which accounts for 62% of the global pie) faced a significant shock with the collapse of the market leader in the venture debt segment. This created a large supply gap in the market. While the demand for private credit from firms continues to grow, the past year has seen the emergence of many smaller banks, alternative lenders, and credit funds step up to extend more private credit at a time when traditional banks have become hesitant to do so. Since the Global Financial Crisis, the amount of money raised for private debt has surged more than 5x times; this significant growth in investor interest has been largely driven by the overall global economic conditions. The period of historically low interest rates resulted in diminished returns from traditional fixed-income investments, making the prospect of earning a premium for holding less liquid loans—potentially up to an additional 300 bps—particularly appealing. As an asset class, private credit has continued to grow exceptionally well, growing by 11% over 2017-22.

Fundraise activity by debt funds is only set to grow – in H2 2023, at least 11 new AIFs have registered with a credit or special situation orientation. The growth in the asset class has been thanks to a variety of lending options that meet the needs of businesses and investors alike. Businesses get custom-made loans, fueling growth through direct lending, mezzanine financing to avoid equity dilution, distressed debt, and subordinated debt as the last lifeline for a company’s recovery. This has especially been an attractive option for financing use-cases that have been outside traditional banks’ underwriting criteria or where there have been regulatory restrictions on financing by banks. Venture debt (VD) has arisen as a new and attractive category among startups that wish to raise non-dilutive capital, extend their runways, and expand their performance metrics to grow into their valuations.

Looking specifically at venture debt, the market has been consistently growing at 34% since 2017, with a notable 50% surge in funding in the last year alone. The VD market in India is still not as deep as its equity counterpart – in 2023, even though the year was very muted for VC/PE activity, India still contributed to 3% of the global VC market ($8 billion.), while it remains at sub-2% for venture debt.

On sectoral trends in the space, fintech leads in receiving VD funding (55% of the total), followed by consumer (26%), however, this trend is reversed in the case of deal counts (23% and 34%), indicating that average ticket sizes for fintech transactions are significantly larger. This trend has carried over in the case of VC/PE equity funding, with financial services standing as the largest sector in 2023 (deal volume and value, ex. real estate and infrastructure), even after having fallen significantly (40%) from the previous year; consumer stand in third place for VC/PE investments in value terms and second in volumes, also despite experiencing a steep fall driven by a fall in funding towards e-commerce startups. In terms of deal count, pre-Series A to Series C deals account for nearly 80% of the total, a shift away from the tradition of funding offered to later-stage companies due to their well-established market presence, scale, profitability, etc.

Private credit as an asset class will only continue to grow, given the rise of investors looking to deploy their wealth into newer, more lucrative asset classes. A benchmark of debt funds of a 3+ year vintage reveals returns broadly in the range of 14%, thus offering at least a 400 bps upside in comparison to traditional debt instruments. The asset class offers attractive returns for institutions and family offices alike, especially considering the regular liquidity enabled through coupon structures.

In conclusion – there are two faces to this asset class. While debt can serve as a crucial source of funding for companies, excessive debt can have detrimental effects.. When the going gets tough, loan traps are not easy to get out of. We’ve recently seen instances of how this has played out in the Indian context as well. Private credit structures that are significantly non-cash-flow based (especially in loss-making companies) are exposed to significant risks around the turning tides of interest rates and the money supply. These structures undertake risks akin to VC and PE investors, while not having the upside potential that equity investors do. As the asset class grows in India, the market will also mature in terms of risk segments, financing structures, and return profiles.